What is the law of demand and how the law works?

The Law of Demand is a fundamental concept in economics that explains the relationship between the price of a good or service and the quantity demanded of that good or service. It is one of the most basic laws of economics, and understanding it is essential to comprehend how markets work. In this blog, we will discuss the Law of Demand in detail, including its definition, explanation, demand curve, price, quantity, relationship, inverse, slopes, factors, consumer behavior, economics, market demand, individual demand, and Law of Supply and Demand. Additionally, we will provide some real-life examples and demand schedules to illustrate the concept.

Definition

The Law of Demand states that as the price of a good or service increases, the quantity demanded of that good or service decreases, while all other factors remain constant. Conversely, as the price of a good or service decreases, the quantity demanded of that good or service increases, while all other factors remain constant. In simple terms, people will buy less of a good or service when its price goes up, and they will buy more of it when the price goes down.

Explanation

The Law of Demand can be explained using the concept of marginal utility. The term “marginal utility” refers to the extra level of satisfaction that a consumer experiences by consuming an additional unit of a product or service. As a consumer consumes more units of a good or service, the marginal utility of each additional unit decreases. Therefore, the consumer is willing to pay less for each additional unit of the good or service. As the price of the good or service increases, the marginal utility of each additional unit decreases more quickly, leading to a decrease in the quantity demanded.

Key Points for the Law of Demand

- The law of demand is a foundational principle in economics, stating that as the price of a good or service increases, the quantity demanded by consumers decreases.

- This relationship is based on the idea of diminishing marginal utility, which means that as consumers acquire more of a good, the additional satisfaction they derive from each unit decreases.

- A market demand curve illustrates the total quantity demanded at each price point by all consumers in the market. While changes in price can lead to movement along the demand curve, they do not directly change the overall level of demand. Instead, changes in consumer preferences, income levels, or the availability of related goods can shift the demand curve, altering the quantity demanded at each price point.

- Therefore, the shape and magnitude of demand depend on factors beyond just changes in price.

The Demand Curve

The demand curve is said to be the graphical representation of law of demand where we take specific quantity of any good in relation to the price. The demand curve shows the relationship between the price of a good or service and the quantity demanded of that good or service, while all other factors remain constant. The demand curve is downward sloping, which means that as the price of a good or service increases, the quantity demanded of that good or service decreases, and a decrease in the price of a product or service results in an increase in the quantity demanded of that product or service.

Relationship of Price and Quantity

The law of Demand illustrated the inverse correlation between the price of a good or service and the quantity demanded. This means that as the price of a good or service increases, the quantity demanded of that good or service decreases, and as the price of a good or service decreases the quantity demanded of that specific good or service increases.

Inverse Slopes

The inverse relationship between price and quantity demanded leads to a downward sloping demand curve. The slope of the demand curve is negative, which means that as the price of a good or service increases, the quantity demanded of that good or service decreases at a decreasing rate.

Factors Affecting Demand

The Law of Demand assumes that all other factors remain constant. However, in the real world, there are several factors that can affect demand, such as consumer income, consumer tastes and preferences, the price of related goods, and the number of consumers in the market.

Consumer Behavior & Law of Demand

Consumer behavior plays a crucial role in the Law of Demand. Consumers are rational beings who seek to maximize their satisfaction with limited resources. As such, they will purchase goods and services based on their marginal utility and willingness to pay. Consumers will buy more of a good or service when its price is lower because they can purchase more of it for the same amount of money.

Law of Demand in The Fields of Economics

In the field of economics, the Law of Demand is a fundamental principle. It forms the basis for understanding how markets work, how prices are determined, and how supply and demand interact.

Market Demand vs. Individual Demand

The Law of Demand applies to both market demand and individual demand. Market demand is the total demand for a good or service in a particular market, while individual demand is the demand for a good or service

The Demand schedule

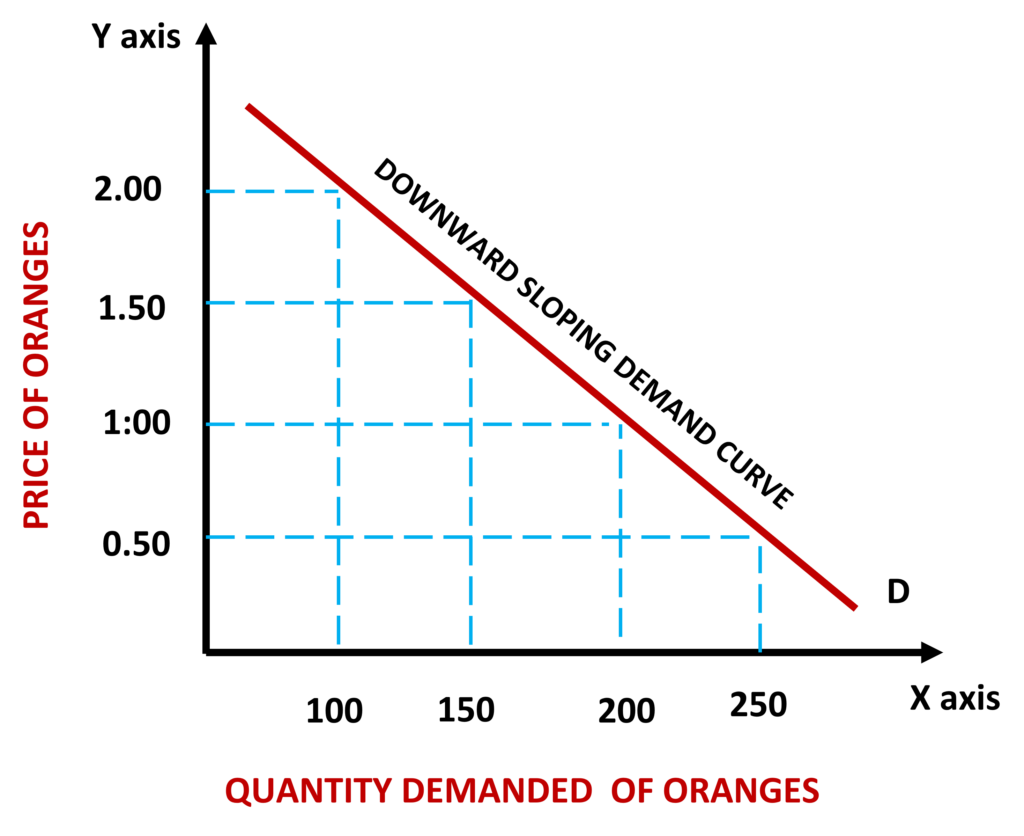

A demand schedule is a table that shows the relationship between the price of a good or service and the quantity demanded of that good or service, while all other factors remain constant. Here is an example of a demand schedule for oranges:

| Price of Oranges ($) | Quantity Demanded (lbs) |

| $2.00 | 100 |

| $1.50 | 150 |

| $1.00 | 200 |

| $0.50 | 250 |

Demand curve

To create a demand curve, we can plot the data points from the demand schedule on a graph with price on the vertical axis (y-axis) and quantity demanded on the horizontal axis (x-axis). Here is the demand curve for oranges using the given data:

In the above demand schedule, as the price of oranges decreases, the quantity demanded of oranges increases. The Law of Demand is demonstrated by this example.

Real-Life Examples of Law of Demand

Real-life examples of the inverse relationship between demand and price can be seen in many markets. Here are some examples:

Gasoline:

When the price of gasoline increases, people tend to drive less or switch to more fuel-efficient vehicles, leading to a decrease in the quantity demanded of gasoline. Conversely, when the price of gasoline decreases, people tend to drive more or switch to less fuel-efficient vehicles, leading to an increase in the quantity demanded of gasoline.

Airline tickets:

When the price of airline tickets increases, people tend to travel less or choose alternative modes of transportation, leading to a decrease in the quantity demanded of airline tickets. Conversely, when the price of airline tickets decreases, people tend to travel more, leading to an increase in the quantity demanded of airline tickets.

Electronics:

When the price of electronics, such as smartphones or laptops, increases, people tend to hold off on purchasing or choose cheaper alternatives, leading to a decrease in the quantity demanded of electronics. Conversely, when the price of electronics decreases, people tend to purchase more or upgrade to more expensive models, leading to an increase in the quantity demanded of electronics.

In each of these examples, we can see that the Law of Demand holds true. As the price of a good or service increases, the quantity demanded of that good or service decreases, and as the price of a good or service decreases, the quantity demanded of that good or service increases.

Conclusion

In conclusion, the Law of Demand is a fundamental principle in economics that describes the inverse relationship between the price of a good or service and the quantity demanded of that good or service. When the price of a product or service decreases, the quantity demanded of that product or service increases, and when the price of a product or service increases, the quantity demanded of that product or service decreases. This principle has important implications for consumer behavior, market demand, and the overall balance of supply and demand in the economy.

References

- Mankiw, N. G. (2014). Principles of microeconomics. Cengage Learning.

- Perloff, J. M. (2018). Microeconomics. Pearson.

- Samuelson, P. A., & Nordhaus, W. D. (2010). Economics. McGraw-Hill.

- Varian, H. R. (2014). Intermediate microeconomics: a modern approach. WW Norton & Company.